This might not even come close to the real distribution and I'm also not going to comment on the usefulness of this endeavor or the final result.

I'll take your data as five points of a CDF assigning kind of arbitrary probability values to the maximum loss and maximum profit values

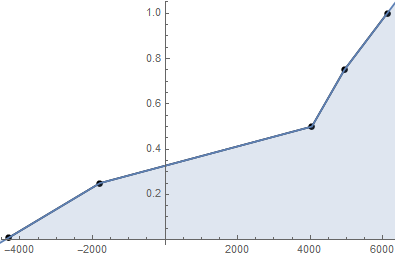

data = {{-4305, 0.01}, {-1801, 0.25}, {4044, 0.5}, {4938, 0.75}, {6120, 1.00}}

and interpolate this data.

if = Interpolation[data, InterpolationOrder -> 1];

listPlot = ListPlot[data, Joined -> True, Mesh -> All, PlotStyle -> Black];

Show[listPlot, Plot[if[x], {x, -5000, 7000}, Filling -> Axis, PlotRange -> All]]

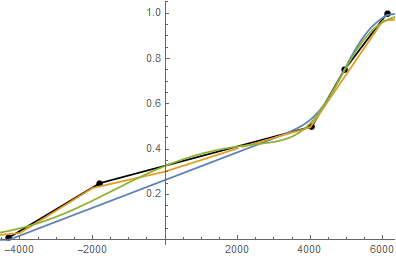

Using the interpolated data (if) to define a ProbabilityDistribution

pD = ProbabilityDistribution[{"CDF", if[x]}, {x, -4305, 6120}, Method -> "Normalize"];

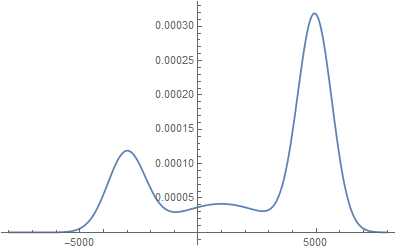

Plot[PDF[pD], x], {x, -5000, 7000}, Filling -> Axis, PlotRange -> All]

Show[{listPlot, Plot[CDF[pD], x], {x, -5000, 7000}, Filling -> Axis, PlotRange -> All]}]

One can use this ProbabilityDistribution (pD) to derive some additional statistics. For example

Through[{Mean, StandardDeviation, Quantile[#, {1/100, 1/4, 1/2, 3/4, 99/100}] &}[pD]]] // N

$\ ${2073.39, 3461.64, {-4201.71, -1625.65, 4061.88, 4949.82, 6073.19}}

Or create some pseudorandom variats from pD

rv = RandomVariate[pD, 100000];

and feed FindDistribution with them

{dist1, dist2, dist3} = FindDistribution[rv, 3]

Show[{listPlot, Plot[{CDF[dist1, x], CDF[dist2, x], CDF[dist3, x]}, {x, -8000, 8000}]}]

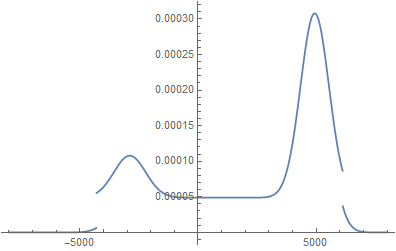

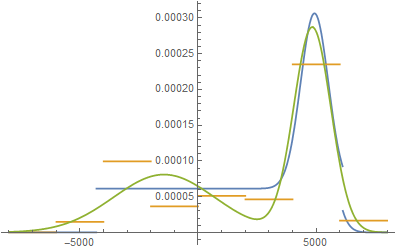

Plot[{PDF[dist1, x], PDF[dist2, x], PDF[dist3, x]}, {x, -8000, 8000}]

Through[{Mean, Median, StandardDeviation, Quantile[#, {1/100, 1/4, 1/2, 3/4, 99/100}]&}[dist1]]

$\ ${2355.22, 3724.49, 3104.68, {-4141.88, -231.04, 3724.49, 4937.08, 6093.1}}

Through[{Mean, Median, StandardDeviation, Quantile[#, {1/100, 1/4, 1/2, 3/4, 99/100}]&}[dist2]]

$\ ${2145.7, 4014.08, 3556.66, {-5328.89, -1409.09, 4014.08, 5077.46, 7396.}}

Through[{Mean, Median, StandardDeviation, Quantile[#, {1/100, 1/4, 1/2, 3/4, 99/100}]&}[dist3]]

$\ ${2102.4, 3907.54, 3468.62, {-5719.51, -1039.81, 3907.54, 4950.12, 6491.02}}

From another run of RandomVariate I got these PDFs: