$Version

(* "13.1.0 for Mac OS X x86 (64-bit) (June 16, 2022)" *)

Clear["Global`*"]

distY = TransformedDistribution[Max[E^(x - 1) - κ, 0],

x \[Distributed] NormalDistribution[μ, σ]];

distY inherits the assumptions from the NormalDistribution

dpa = DistributionParameterAssumptions[distY]

(* μ ∈ Reals && σ > 0 *)

pdf[y_] = PDF[distY, y]

(* 1/2 DiracDelta[

y + κ] (1 +

Erf[(1 - μ + Log[y + κ])/(Sqrt[2] σ)]) UnitStep[y] - (

E^(-((1 - μ + Log[y + κ])^2/(2 σ^2)))

UnitStep[y] (-1 + UnitStep[-y - κ]))/(

Sqrt[2 π] (y + κ) σ) -

1/2 DiracDelta[

y] (1 + Erf[(1 - μ + Log[κ])/(Sqrt[2] σ)]) (-1 +

UnitStep[-κ]) *)

Checking the total probability (this is quite slow),

AbsoluteTiming[

Assuming[dpa, Integrate[pdf[y], {y, -Infinity, Infinity}] // Simplify]]

(* {40.1147, ConditionalExpression[1, Re[κ] >= 0 && Im[κ] == 0]} *)

Consequently, this requires κ >= 0 and

distY = TransformedDistribution[Max[E^(x - 1) - κ, 0],

x \[Distributed] NormalDistribution[μ, σ],

Assumptions -> κ >= 0];

dpa = DistributionParameterAssumptions[distY]

(* κ >= 0 && μ ∈ Reals && σ > 0 *)

pdf[y_] = PDF[distY, y]

(* 1/2 DiracDelta[

y] (1 + Erf[(1 - μ + Log[κ])/(Sqrt[2] σ)]) - (

E^(-((1 - μ + Log[y + κ])^2/(

2 σ^2))) (-1 + UnitStep[-y]))/(Sqrt[2 π] (y + κ) σ) *)

Assuming[dpa, Integrate[pdf[y], {y, -Infinity, Infinity}]]

(* 1 *)

This is a mixed distribution with a discrete probability for y == 0 of

pdf2[0] = 1/2*(1 + Erf[(1 - μ + Log[κ])/(Sqrt[2]*σ)]);

and a continuous probability distribution for y > 0 of

pdf2[y_] = ConditionalExpression[

Simplify[-((-1 + UnitStep[-y])/

(E^((1 - μ + Log[y + κ])^2/(2*σ^2))*

(Sqrt[2*Pi]*(y + κ)*σ))), y > 0], y > 0]

(* ConditionalExpression[

1/(E^((1 - μ + Log[y + κ])^2/(2*σ^2))*

(Sqrt[2*Pi]*(y + κ)*σ)), y > 0] *)

Assuming[dpa,

pdf2[0] + Integrate[pdf2[y], {y, 0, Infinity}] //

FullSimplify]

(* 1 *)

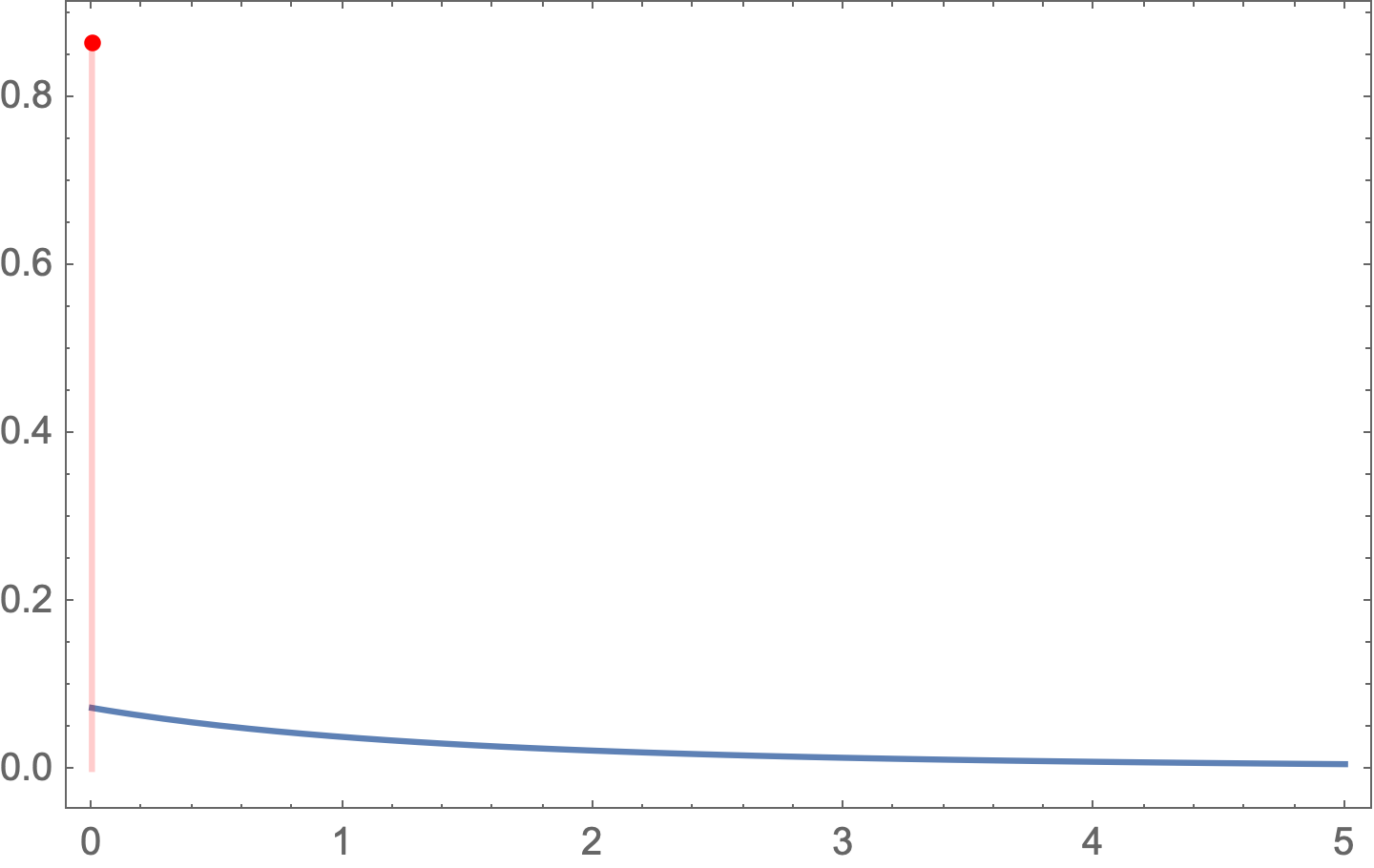

Plotting,

μ = 1; σ = 1; κ = 3;

Show[

Plot[pdf2[y], {y, -1/2, 5}],

DiscretePlot[pdf2[y], {y, 0, 0},

PlotStyle -> Red],

PlotRange -> All,

Frame -> True,

Axes -> False]