The time series that FinancialData creates has the option TemporalRegularity -> Automatic. With this option, this series does not interpolate values.

data =

FinancialData["SBUX", "Close", {{2013, 1, 1}, {2013, 8, 1}, "Week"}, "Value"];

Time series that aren't regularly sampled can interpolate values with the option TemporalRegularity -> True. To demonstrate, let's use TimeSeries to make a list of dates between two of the data samples. Change the data time series to assume regular time samples with TemporalRegularity -> True.

{dt1, dt2} = data["Dates"][[9;;10]];

dates = DateRange[dt1, dt2];

ts = TimeSeries[data, TemporalRegularity -> True];

The data series does not interpolate values.

data[dates]

{$27.43, $27.43, $27.43, $27.43, $27.43, $27.43, $27.43, $29.33}

With TemporalRegularity -> True, the ts series linearly interpolates values for dates between samples.

ts[dates]

{$27.43, $27.71, $27.98, $28.25, $28.52, $28.79, $29.06, $29.33}

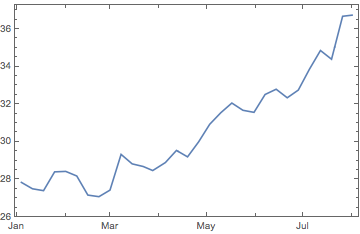

To get evenly-spaced interpolated values for the entire time series, use the first and last dates of the series for the list of dates. With these new dates, ts[dates] gives regular, evenly-spaced values. Here's a plot of the interpolated values.

ts = TimeSeries[data, TemporalRegularity -> True];

{dt1, dt2} = ts /@ {"FirstDate", "LastDate"};

dates = DateRange[dt1, dt2];

DateListPlot[Transpose[{dates, ts[dates]}]]