Using the Temporal Data Framework

While Cashflow is a nice feature for doing financial calculations it lacks the powerful functionality to process time series that has been built into Mathematica as of Version 10 and later.

Using this framework we can convert the cashflows into event series (which essentialy is what they are) and can then use TimeSeriesResample to align the cashflows and add them up correctly.

Implementation

addCashflows[ cashflows : { __Cashflow} ] := Module[

{

minTime,

maxTime,

minTimeInc,

timeSeries

},

(* convert the cashflows *)

timeSeries = EventSeries[ #, MissingDataMethod -> {"Constant", 0} ]& @@@ cashflows;

(* find the parameters to align the event series *)

{ minTime, maxTime, minTimeInc } = timeSeries // RightComposition[

Map[ {#["FirstTime"],#["LastTime"], MinimumTimeIncrement @ # }& ],

Transpose,

Apply[ { Min @ #1, Max @ #2, Min @ #3 }& ]

];

(* align event series, add them and return the total cashflow *)

timeSeries // RightComposition[

Map[ TimeSeriesResample[ #, { minTime, maxTime, minTimeInc }] & ],

Total,

Normal,

Cashflow

]

]

To make all this more comfortable and in the end "more elegant" we can overload the definition for Cashflow:

Unprotect[ Cashflow ];

Cashflow/: Times[ a_ , Cashflow[ c_?VectorQ ] ] := Cashflow[ a c ]

Cashflow/: Times[ a_ , Cashflow[ c_?VectorQ, q_ ] ] := Cashflow[ a c, q ]

Cashflow/: Times[ a_ , cashflow : Cashflow[{ { _ , _ }.. }] ] := Apply[

Function[ { time, value }, {time, a value} ],

cashflow,

{2}

]

Cashflow/: Plus[ cashflows__Cashflow ] := { cashflows } // RightComposition[

ReplaceAll[

{

Cashflow[ c_?VectorQ ] :> Cashflow[

Transpose @ { Range[ 0, Length @ c - 1], c }

],

Cashflow[ c_?VectorQ, q_?NumericQ ] :> Cashflow[

Transpose @ { NestList[ # + q & , 0 , Length @ c - 1 ], c }

]

}

],

addCashflows

]

Protect[ Cashflow ];

Testing the Functionality

Now we can test the functionality using the OP's data.

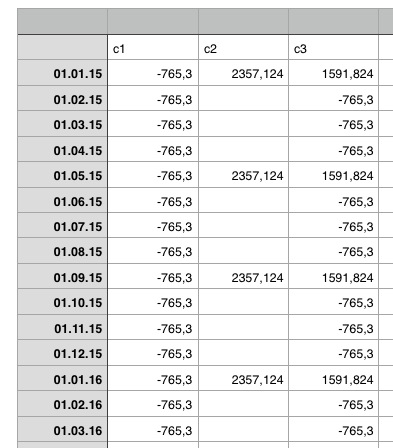

c1 = Cashflow[ Annuity[-765.3, 4, 1/12] ] (* monthly payments_ *)

c2 = Cashflow[ Annuity[2357.124, 4, 1/4 ] ] (* quarterly payments *)

totalCF = c1 + c2;

totalCF // First // Dataset

We can now also subtract cash flows:

c1 - c2

Cashflow[{{1/12, -765.3}, {1/6, -765.3}, {1/4, -3122.42}, {1/

3, -765.3}, {5/12, -765.3}, {1/2, -3122.42}, {7/12, -765.3}, {2/

3, -765.3}, {3/4, -3122.42}, {5/6, -765.3}, {11/

12, -765.3}, {1, -3122.42}, {13/12, -765.3}, {7/6, -765.3}, {5/

4, -3122.42}, {4/3, -765.3}, {17/12, -765.3}, {3/2, -3122.42}, {19/

12, -765.3}, {5/3, -765.3}, {7/4, -3122.42}, {11/6, -765.3}, {23/

12, -765.3}, {2, -3122.42}, {25/12, -765.3}, {13/6, -765.3}, {9/

4, -3122.42}, {7/3, -765.3}, {29/12, -765.3}, {5/2, -3122.42}, {31/

12, -765.3}, {8/3, -765.3}, {11/4, -3122.42}, {17/6, -765.3}, {35/

12, -765.3}, {3, -3122.42}, {37/12, -765.3}, {19/6, -765.3}, {13/

4, -3122.42}, {10/3, -765.3}, {41/12, -765.3}, {7/

2, -3122.42}, {43/12, -765.3}, {11/3, -765.3}, {15/

4, -3122.42}, {23/6, -765.3}, {47/12, -765.3}, {4, -3122.42}}]

We can now also work with short forms of Cashflow:

Cashflow[ {1,2,3} ] + Cashflow[ {1,2,3}, 2 ]

Cashflow[{{0, 2}, {1, 2}, {2, 5}, {3, 0}, {4, 3}}]

Flatten@Riffle[c2, {{0, 0, 0}}, {2, 2 Length[c2], 2}]$\endgroup$Cashflowusing your approachFlatten@Riffle[c2[[1,All,2]],{{0,0,0}},{2,2 Length[c2[[1]],2}]$\endgroup$TimeSeriesAggregatedoes have a very concise meaning which is quite different. $\endgroup$