I have read these two Q&A:

PDF of the product of two independent Gamma random variables

How to Plot the PDF of Product of two Normals

I have two correlated Meixner random variables, $X$, and $Y$, where

$\qquad X\sim MXN(a=0.03306, b=0.30800, m=-0.00099, d=0.44168)$, $\qquad Y \sim MXN(a=0.03064, b=0.45599, m=-0.00173, d=0.51881)$

I need compute the product distribution the $Z=X \cdot Y$. The joint distribution of $X$ and $Y$ is the Student's $t$ copula model with two parametrs: correlation $\rho=0.722$ and degree of freedom $v=7.566$.

I have tried

Z =

TransformedDistribution[x*y,

{x \[Distributed] MeixnerDistribution[0.03306, 0.30800, -0.00099, 0.44168],

y \[Distributed] MeixnerDistribution[0.03064, 0.45599, -0.00173, 0.51881]}]

and TransformedDistribution gives Mean[Z]=2.50021*10^-6 output only.

Edit

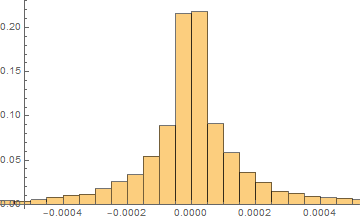

I have tried Plot[PDF[Z, x], {x, 0, 1}] but the Mathematica software v.10 is running. I'm looking for the theoretical solution.

Question

How to compute the product distribution of two Meixner variables?

MeixnerDistribution[]ought to be positive. Maybe check if the definition you're using matches Mathematica's? $\endgroup$