I have a homework project. I need to analyse a gambler's ruin where there are 6 possible outcomes of every wager with corresponding probabilities and payoffs and the gambler may vary the wager (say only 4 values). Am I correct in thinking the gambler's wealth (say 0 to 200 starting at 100) is a 2D random walk with unequal steps. The state space having bankroll on one axis and wager value on the other with bankroll increment determined by outcome, payoff and wager. I can easily simulate this in Excel (or Mathematica) but that won't provide the necessary ruin insight. I could do repeated simulations in Excel stopping at ruin and then derive an empirical PDF of ruin. Mathematica seems to have only 1D RW with equal steps

$\begingroup$

$\endgroup$

10

-

$\begingroup$ I was looking for a built in function, something analogous to DiscreteMarkovProcess, where I can then interrogate the function regarding stopping, ruin etc. Actually generating a walk (as in a single simulation realisation) is trivial, I can write a macro in excel in 5 minutes. But I am a newbie to Mma and the documentation is very dense in places. $\endgroup$– PatrickCommented Jan 28, 2014 at 8:10

-

$\begingroup$ Also your example looks like it has unit steps $\endgroup$– PatrickCommented Jan 28, 2014 at 8:13

-

$\begingroup$ And equal probabilities. I need to use 6 different probabilities and the payoffs are not all even money, hence the wealth increments are unequal. $\endgroup$– PatrickCommented Jan 28, 2014 at 8:37

-

$\begingroup$ For fixed wagers the problem is also trivial as I can construct a transition matrix to feed into DiscreteMarkovProcess with absorbing states (probability 1) at 0 and 200 corresponding to ruin and doubling wealth respectively. I can then interrogate the function to get ruin/doubling probabilities and other stuff. How do I accomplish the same thing with varying wagers. $\endgroup$– PatrickCommented Jan 28, 2014 at 8:55

-

$\begingroup$ How is the wage going to vary along the process? $\endgroup$– Dr. belisariusCommented Jan 28, 2014 at 10:44

|

Show 5 more comments

1 Answer

$\begingroup$

$\endgroup$

$\endgroup$

Here you have a boilerplate for coding the simulation. I've filled each function with a "reasonable random" behavior for a betting game that follows your experiment description. You should customize them to fit better your simulation needs.

I can't infer from your question what are the random vars for your PDF, but the outcome from the function lets you get (I think) any statistic you may want:

allowedWagers[] := {1, 2, 3, 4};

wagerAmount[currentBankRoll_, lastResult_] := Module[{r},

While[(r = RandomChoice[allowedWagers[]]) > currentBankRoll]; r]

stopCondition[initialBankRoll_, currentBankRoll_] := Module[{},

Which[

currentBankRoll < Min@allowedWagers[], 0, (* 0 == Ruin *)

currentBankRoll == 2 initialBankRoll, 1, (* 1 == Won *)

True, 2 (* 2 == Continue *)

]

]

diceF[] := Module[{}, RandomChoice@Range@6]

payOff[dice_] := Module[{payoffs = {-1, -.5, -.2, .2, .4, 1}},(*returns the % gain/loss*)

payoffs[[dice]]

]

doWalk[initialBankRoll_] := Module[{lastResult = 1, bankRoll = initialBankRoll,

walk = {}, wa, sc, lr},

While[

(sc = stopCondition[initialBankRoll, bankRoll]) == 2,

(bankRoll = bankRoll + (wa=wagerAmount[bankRoll, lastResult]) payOff[lr = diceF[]];

lastResult = lr;

AppendTo[walk, {bankRoll, wa}])];

Return@Append[walk, {sc}]

]

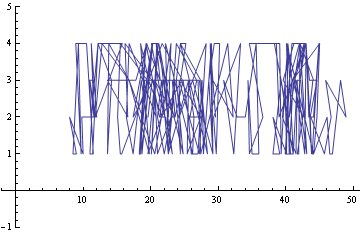

The "states space" random walk you mentioned in the question:

initialBankRoll = 20;

SeedRandom[42];

ListLinePlot[Most@doWalk[initialBankRoll], PlotRangePadding -> {2, 1}, AxesOrigin -> {0, 0}]

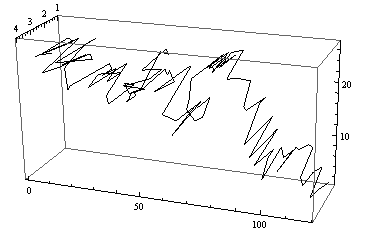

The same, viewed as a time-evolution process:

initialBankRoll = 20;

SeedRandom[42];

Graphics3D[Line@(Prepend@@@ (Transpose@{#,Range@Length@#} &@Most@doWalk[initialBankRoll])),

BoxRatios -> {10, 5, 3}, Axes -> True]

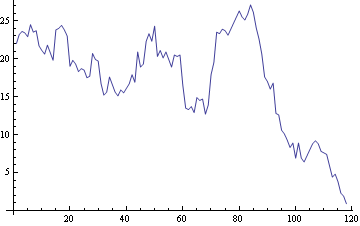

The evolution of the bank roll:

initialBankRoll = 20;

SeedRandom[42];

ListLinePlot[Most[doWalk[initialBankRoll][[All, 1]]]]

answered Jan 28, 2014 at 21:46